‘Pension Builder’ launched by interactive investor

28th February 2022 08:00

by Jemma Jackson from interactive investor

Share on

Our low-cost, standalone Pension Builder plan is aimed at the 6.2 million people in the UK who want to build up their long-term wealth by focusing on their pension.

- New research reveals 8 million UK adults don’t think pension admin costs even exist, but they can add up to tens of thousands of pounds over the long term

- Analysis highlights eye-watering differences between pension providers

- It “breaks the mould completely” says Richard Wilson, CEO, interactive investor

interactive investor, the UK’s second-largest DIY investment platform and number one flat fee provider, has today launched a game-changing standalone pension – a Self-Invested Personal Pension (SIPP) called Pension Builder.

For a flat fee of just £12.99 per month, interactive investor’s Pension Builder plan is squarely aimed at the 6.2 million people in the UK who want to build up their long-term wealth by focussing on their pension*.

- Invest with ii: What is a SIPP? | Is a SIPP right for me? | SIPP Cashback Offers

Pension Builder comes with free monthly investing and the full, market leading choice of investments. So, for those who don’t want an ISA, and don’t trade regularly, it’s incredibly good value – as the table below demonstrates. And from just over £100,000 the Pension Builder even beats Vanguard.

Richard Wilson, CEO, interactive investor, says: “Our pension price was amazing before. Now, at only £12.99 a month to run your pension, it breaks the mould completely.

“We are proud to launch this low cost, flat fee Pension Builder. What you see is what you get – a transparent charge in pounds and pence that stays the same as your wealth grows. We’ve designed this product to make building your pension pot simple, straightforward, and ultimately - satisfying. You can take true ownership of your pension and help shape the retirement life you aspire to.”

The truth behind percentage fees

Surprisingly, 8 million of adults in the UK don’t think pension admin costs exist, according to ii research conducted by Opinium. And many struggle to work out the impact of percentage fees.

To put ii’s £12.99 per month Pension Builder into context, interactive investor, with help from platform consultancy Compare the Platform, has looked at how some of its competitors compare, converting their percentage fees into an equivalent monthly fee for comparative purposes.

interactive investorPension Builder customers pay a flat £12.99 per month regardless of the size or composition of their investment. For some smaller pensions that might look steep, but as your pension builds up, this flat fee comes into its own.

Assuming a pension portfolio split 50/50 between funds and equities in a £100,000 pension pot, Hargreaves Lansdown pension customers would pay £36.92 per month; £19.83 with Fidelity Personal Investing and £23.42 with AJ Bell YouInvest. As the table below shows, as pot sizes increase, so too do the charges. Investors with a £250,000 pension pot are paying £65 per month in charges with ii’s largest competitor.

Portfolio value | £50,000 | £100,000 | £150,000 | £200,000 | £250,000 |

interactive investor (Pension Builder) | £ 12.99 | £12.99 | £12.99 | £12.99 | £12.99 |

Fidelity Personal Investing | £12.54 | £19.83 | £27.13 | £34.42 | £26.08 |

AJ Bell YouInvest | £13.42 | £23.42 | £28.63 | £33.83 | £39.04 |

Barclays Smart Investor | £20.75 | £27.00 | £33.25 | £39.50 | £45.75 |

Hargreaves Lansdown | £20.25 | £36.92 | £46.29 | £55.67 | £65.04 |

The examples above are based on 50/50 funds and direct equities, with one regular fund investment, and one regular share investment each month, reflecting the fact that the average interactive investor customer has a mix of each in their portfolio. The table does not include fund charges, and is platform costs only.

However, assuming 100% funds, it is interesting to see how Vanguard compares. Vanguard equates to £6.25 per month for a £50,000 pot and £12.50 per month for a £100,000 pot. From £104,000, interactive investor become cheaper (assuming only regular investments), with Vanguard’s costs rising to £18.75 for a £150,000 pot, and rising to £25 per month for a £200,000 pot and £31.25 for a £250,000 pot.

Years and years

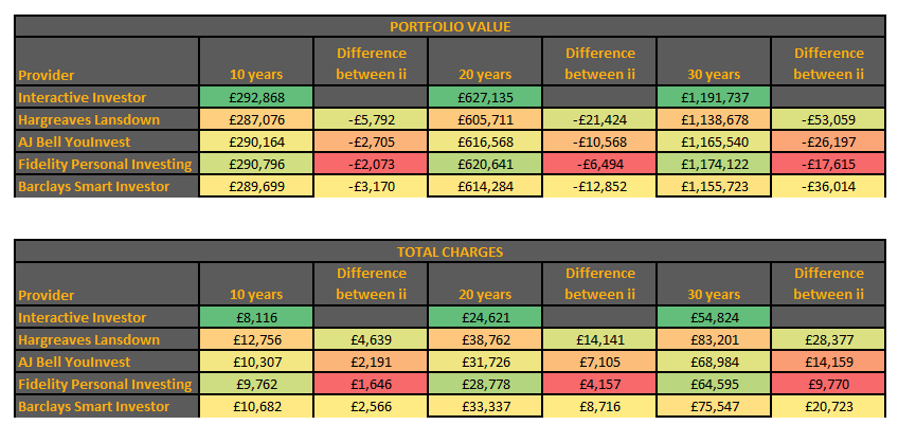

Over the long term, the differences between interactive investor’s Pension Builder and its competitors’ stand-alone pensions is thought provoking and could add up to tens of thousands of pounds. The difference in retirement pot size with ii could literally add years to some retirement pots. See notes to editors** for illustrations.

Homing in on pensions

Becky O’Connor, Head of Pensions and Savings, interactive investor, says: “We know millions of people would like to boost their retirement pots because they are not currently on track to be able to give up work and have a good standard of living when they do. We also know more people are becoming more confident about managing their pension investments for themselves. The low flat fee on the Pension Builder means that cost savings you make compared to other platforms can contribute to your future instead. Over the years, the amount saved could add thousands of pounds to your retirement income. Many people in the UK do not get close to using up their annual allowance of £40,000 a year or up to their maximum level of earnings, so have plenty of room to go for it on pension contributions if they are prioritising retirement.”

Key features of Pension Builder:

- Same breadth and depth of choice – funds, investment trusts, ETFs, and direct equities (UK, US and international shares across 17 global exchanges)

- Simple and low-cost pricing - £12.99 a month

- Trading costs: £7.99 for UK shares and ETFs, funds, investment trusts and US shares. Other international shares £19.99. Dividend reinvestment 99p

- Free monthly investing into funds, investment trusts, ETFs and popular UK shares

- No free trading credit

- More visibility over your pension, with an accessible and easy to use app

- Easy to use select lists, model portfolios, quick start funds and more

- Calculators to help you plan your retirement

- Customers can upgrade to also have an ISA, trading account, as many free Junior ISAs as they have children, and one free trade a month, for just £7 per month extra

- Until ii launched Pension Builder, customers wanting just an ii pension would pay a £10 per month SIPP fee, and a £9.99 per month ii subscription fee which comes with a trading account, ISA and as many free JISAs as customers have children.

- First 6 months subscriptions on Pension Builder will be free for all new customers

Flat fees innovation

In 2019 interactive investor introduced its innovative, ‘Netflix style’ monthly subscription fee pricing. In 2020, we introduced free monthly investing for funds, investment trusts, ETFs and popular UK shares and scrapped the £10 per month income drawdown fee on our pension, along with a host of other pension fees. Last year ii launched Friends and Family, allowing our customers to gift a free ii subscription to up to 5 people for just £5 per month.

Becky O’Connor, Head of Pensions, interactive investor, continues: “Pensions are probably the most important long-term saving you will make in your life – and paradoxically, they are often the most overlooked and misunderstood.

“Although it is great to see more people getting excited about investing – the biggest buzz usually surrounds the latest ‘hype.’ More conversations need to be had about meaningful, long-term savings, which the future ‘you’ will thank ‘you’ for.

“Many people are still unaware that a Self-Invested Personal Pension Plan, or SIPP, could be a great option for them. SIPPs offer the same tax advantages as a standard pension, but you have added control over the investments made.”

Puzzled about pensions?

To get a better understanding of how UK savers are approaching their pensions, interactive investor asked savers how they are prioritising their savings, and how clued-up they feel on their current pension pots.

Drip, drip, drip – future financial security going down the drain?

ii has long advocated for the importance of being transparent about how fees and charges can eat into savers’ pockets on a month-by-month basis. The reality of fees cannot be overlooked – and as the years roll into decades, can make a significant impact on savers’ long-term financial health, even if they don’t seem like a lot initially.

Opinium research for ii asked UK adults what a 0.5% percentage fee structure on a £50,000 pot would equate to in the first year of an investment. It was encouraging to see 56% of respondents correctly answered £250 – but that also means that over two fifths of UK adults are unable to work out how much percentage fees are costing them.

But what about charges relating to pension pots? Within the same research, UK adults were asked: Thinking about charges in relation to pension administration costs, which of these most applies to you? 15% of UK adults admitted they did not know that you get charged admin costs for pensions.

Other responses included:

- I don’t look at charges because there’s not a lot I can do about it anyway – 14%

- I look carefully at pension admin costs – they can add up over the long term to large amounts so it’s worth shopping around – 12%

- I never or rarely look at pension admin costs but I have a feeling that I should – 9%

- And of course, the cost of living has had a clear impact on how savers are thinking about their pension charges – with 6% responding ‘I am going to start looking more at pension costs and comparing charges because of the cost of living/ inflation squeeze.’

Notes to Editors

*Source: Opinium Research for interactive investor. Opinium askedpeople are prioritising their savings. 12% are prioritising pensions and Opinium converted this into number of people in the population. Full breakdown below:

Question: Where do you prioritise your saving?

Savings account | 43% |

ISA - cash | 15% |

Pension | 12% |

ISA - stocks and shares | 10% |

Crypto | 1% |

Other | 1% |

I don’t have savings | 18% |

Opinium Research was conducted on behalf of interactive investor between 24th - 25th January 2022 with a sample size: 2,000 UK adults weighted to be nationally representative.

**The differences that charges make to outcomes over the long-term is thought provoking. For example, let’s look at a hypothetical accumulated £100,000 retirement pot at aged 35. With £10,000 annual gross contributions, split into monthly investments, over 30 years (and with 5% annual growth, which is by no means guaranteed), this now 65 year old would have a portfolio value at ii worth £1,191,737 – but with ii’s largest competitor, it would be worth £53,000 less.

The data is from Lang Cat** and assumes a 50/50 between funds and direct equities, a typical investor aged 35 making annual gross contributions of £10,000 split into monthly investments, also on a 50/50 funds/ equities basis.

Lang Cat data assumes 4 trades in each year (2 funds/2 equity) with associated dealing charges included.Fee inflation of 2% per year is factored in.The investment returns reflect the following charges:administration fees, dealing costs (assuming online transactions only), Fund manager charges, known as the Ongoing Charges Figure, at 0.66%.

All competitor charges were taken from their published fees and were correct as at 29 September 2021.

These articles are provided for information purposes only. Occasionally, an opinion about whether to buy or sell a specific investment may be provided by third parties. The content is not intended to be a personal recommendation to buy or sell any financial instrument or product, or to adopt any investment strategy as it is not provided based on an assessment of your investing knowledge and experience, your financial situation or your investment objectives. The value of your investments, and the income derived from them, may go down as well as up. You may not get back all the money that you invest. The investments referred to in this article may not be suitable for all investors, and if in doubt, an investor should seek advice from a qualified investment adviser.

Full performance can be found on the company or index summary page on the interactive investor website. Simply click on the company's or index name highlighted in the article.